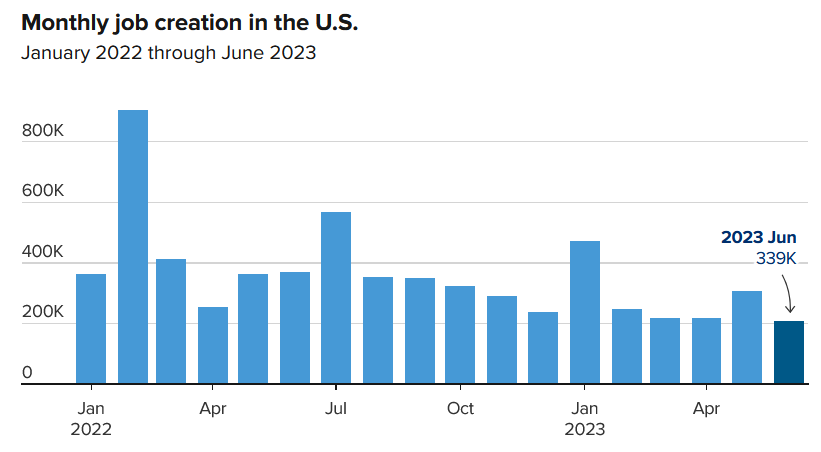

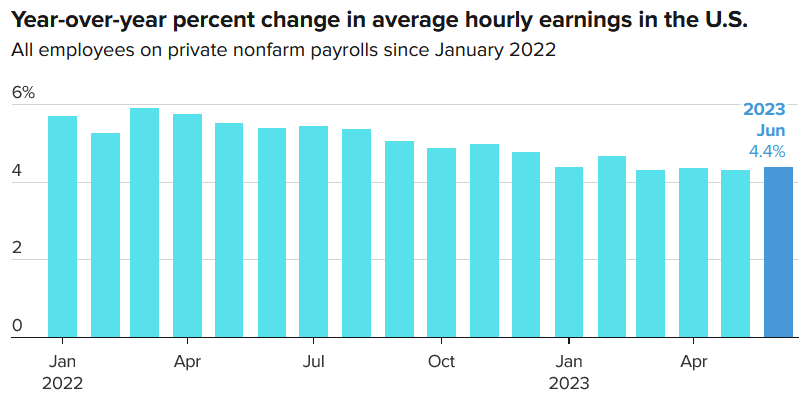

On July 6, 2023, ADP released their monthly private payroll job information. The private sector added 497,000 jobs in June 2023, more than expected, led by gains in the leisure & hospitality and construction sectors. Private Sector wages rose 6.4% year-over-year in June, down slightly from +6.6% year-over-year in May, but still the largest source of sticky inflation in the entire financial system. Today, however, the US Bureau of Labor Statistics (BLS) said that total payrolls rose by 209,000 jobs, less than the 240,000 expected. Overall unemployment remained unchanged at a lowly 3.6%, and the overall labor participation rate was 62.5%. Overall wages in June grew 4.4% year-over-year, slightly more than expected. While monthly job creation and growth in average hourly wages have both slowed modestly, they are still strong overall.

Chart: Gabriel Cortes / CNBC

Source: U.S. Bureau of Labor Statistics via FRED

Chart: Gabriel Cortes / CNBC

Source: U.S. Bureau of Labor Statistics via FRED

The main point is that the job market remains strong overall, it is still the primary source of ‘sticky inflation’ filtering into the rest of the US economy, and the Fed’s substantial efforts to tame inflation with 10 rate hikes since early 2022 (and an 11th coming in July) have not sufficiently slowed the US economy to tame inflation fully. So, we do expect at least two more Fed rate hikes this summer and fall and for rates to stay higher longer than we expected 3-6 months ago. This is disappointing to us, as higher rates widen the multifamily Seller vs. Buyer price divide and make buying multifamily deals overall more challenging and difficult to navigate.

Rate expectations have grown meaningfully in the past three and six months.

As seen below, rate expectations have widened significantly over the past three and six months. Six months ago, there was a 40% chance that the Federal Funds rate would be 400bps or less following the March 2024 Fed meeting and almost a zero chance that Federal Funds rates would be 500bps or more. Today, there is a zero chance that Federal Funds rates will be 400bps or less following the March 2024 Fed meeting and a 91% chance that they will be 500bps or more. This is roughly an 80bps increase in rate expectations over the past three to six months!

Federal Funds Rate Expectations for Mar’24 Fed Meeting Have Widened

Source: Avid Realty Partners and CMEGroup.com

Normalized 10-Year Treasury yield is 1.4% – 3.1%, less than today’s 4.0%.

As seen below, the 10-year US Treasury is now yielding 4.04%, 18bps below the 15-year high of 4.22% achieved in October 2022, and essentially at or near highs not seen since April 2007 when the 10-year yielded 5.05%. In general, we believe that 10-year treasury yields are returning to normalized levels seen from 2008-2019, with this normalized range of 1.4% – 3.1%, less than today’s 4.0%. The US has significantly more federal debt as a percentage of GDP than ever before (120% of GDP today versus 31% of GDP in 1980), and thus we think it is unlikely that US rates will stay so high for so long…cheap debt has fueled the US’ growth strategy for decades, and there is no way around this for a country with high debt levels and declining birth rates (even with the influx of immigration). Further, with SO MUCH federal debt now, the US cannot even afford to keep paying such high rates for so long, even if it wants to. Per below, 10-year Treasury rates fell below trend during Covid — to stabilize the economy — and now are above trend post-Covid to fight inflation as a consequence of over-easing during Covid.

10-Year Treasury Rates for the past 22 Years: Below Trend during Covid and now Above Trend post-Covid

Multifamily debt pricing sets valuation levels, along with construction costs.

In general, we think that multifamily apartment asset pricing is set by overall borrowing cost levels (Fannie Mae and Freddie Mac loans) and by overall construction costs. Our view is that long-term 10-Year Treasury Rates are 1.4% – 3.1% and that Fannie/Freddie debt costs are ~180-200bps wide of Treasuries, suggesting long-term multifamily borrowing costs of 3.2% – 5.1% over the long term, with a midpoint borrowing cost of 4.1%. We also believe that institutional quality multifamily deals trade at or near the cost of debt so that long-term cap rates are quality assets that will range in the same 3.2% – 5.1% range, with a midpoint of 4.1% over the long term. So, buying true 5-cap assets today, and increasing their yield performance to 6.5% yield to total cost, will be a HIGHLY profitable venture in the coming years.

Ride the Wave of Multifamily Investing and Maximize Your Multifamily Investment Returns

Intrigued? Eager to discover more about the multifamily investment world and how it could bolster your portfolio? Schedule your free strategy call with us today! It’s time to move beyond mere understanding and dive into action. Navigate the thrilling twists and turns of multifamily investments, guided by our expert advice. Your journey to financial prosperity is only a click away. Don’t hesitate. Seize the day; seize the opportunity!

In conclusion, we see that inflation is coming down to more normalized levels (slowly), though robust payroll and labor trends are causing some reverberations throughout the economy, thus lessening the fall of inflation in the near term. Due to this, interest rates will stay higher for longer in 2023 and into 2024 before falling to more normalized levels. Elevated rates will cause some distress in the multifamily sector, despite overall sound fundamental performance. Ultimately, lower borrowing costs and still rising construction costs mean that multifamily replacement costs and sales prices will continue to rise, with valuations likely to grow meaningfully in late 2024 and 2025 as the interest rate environment normalizes.

Founder & CEO of Avid Realty Partners. Craig has been an active real estate investor for nearly 20 years, and founded Avid Realty Partners in 2015 to deploy capital across Multifamily Apartment and other real estate assets. Avid Realty Partners’ portfolio includes the acquisition of more than 2,000 apartment and hotel doors in targeted growth markets across the US totaling over $275M of acquisition value. The firm has zero realized losses with a 33.0% IRR (weighted average) across six exited deals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment