Key Multi-Family Apartment Indicators

Key Apartment indicators show solid underlying fundamentals. Here we examine key MFU apartment trends put together by Marcus & Millichap including Supply/Demand, Vacancy Rates, Rental Rates, and others. We conclude that MFU Apartment market fundamentals remain solid, though they are underpinned by a relatively weak US Consumer. Rental Rate increases have been strong, newly built supply is being absorbed into the market at a reasonable pace, and overall US Vacancy Rates are near modern historic lows. While we are not commenting on property or market valuations, which seems stretched due to low interest rates and low cap-rates, key property fundamentals driven by apartment renters appear solid for now.

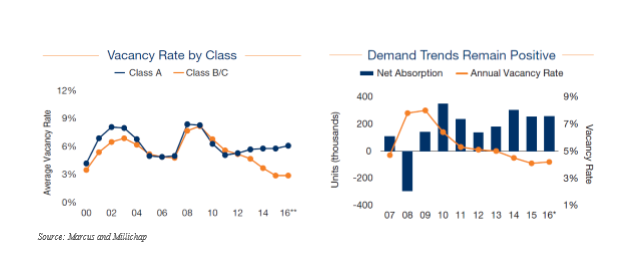

Figure 1. Multi-Family Apartment Vacancy Rates Very Low; Indicates Strong Demand

Source: Marcus and Millichap

Vacancy Rates near modern historic lows, indicating strong demand from Renters. Here we see that Class B/C vacancy rates in particular are quite low, at near 3% overall. Class A vacancy rates are not as low given the new supply that has been ramping into the market in recent years, but still hover around 6%.

Figure 2. Multi-Family Apartment Vacancy Rates Low

Source: FredStLouisFed.org

Different data set shows Vacancy Rates Low and at Levels Not seen since the mid-1980s. Looking at a different data set on apartment rental Vacancy Rates shows that vacancies are down to 7% overall, levels not really seen since the mid-1980s. With ramping supply, particularly in Class A apartments, we think vacancies could begin to rise slightly, but will still remain in normal’ levels seen from 1985-2000.

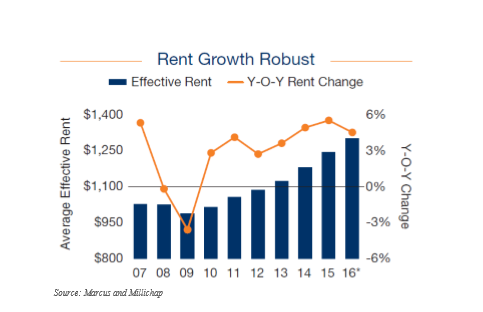

Figure 3. Rental Rates Growing Robustly; May See Falling Growth Rates in 2017-2019

Source: Marcus and Millchap

MFU Apartment Rental Rates have grown robustly since the Downturn; Growth rates could moderate in 2017-2019. National MFU Apartment Rental Rates grew roughly 6% in 2015, a very strong performance and marking the sixth year in a row with growth at or above 3%, according to Marcus & Millichap. We see that average apartment rates have increased significantly from about $1025 in 2007-2008 before the Great Recession to roughly $1300 in 2016. This is a 27% increase in eight years! We do expect that Rental Rates will continue to grow over time, and that average effective rents can be pushed higher as more Class A apartments come online in coming years. However, we also expect that Class B/C rental rate growth could moderate in coming years closer to sustainable price hikes of 2% per year.

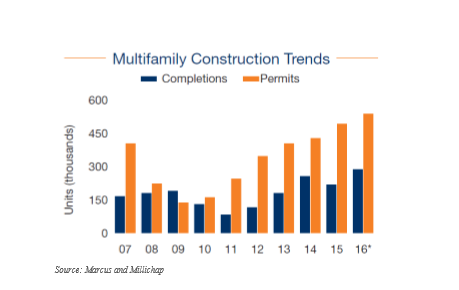

Figure 4. Construction Trends Show Ramping MFU Builds and Supply

Source: Marcus and Millichap

MFU Apartment Supply is ramping given robust rental market metrics, and a lack of new construction builds in 2010-2012. Looking at the data above, we see that MFU Apartment construction and supply has ramped sharply since the below consumption trends seen in 2010-2012. With MFU Apartment demand growing as more Millennials rent instead of own, and with Rental market metrics robust (rising rental rates and low vacancies), developers are motivated to build, ramp supply, and close the gap. We see that many projects are being permitted, and that actual MFU supply delivered to the market is growing strongly. These trends suggest that low Vacancy Rates will rise somewhat, and the heady Rental Rate increases seen in 2014-2016 could moderate some or level off entirely.

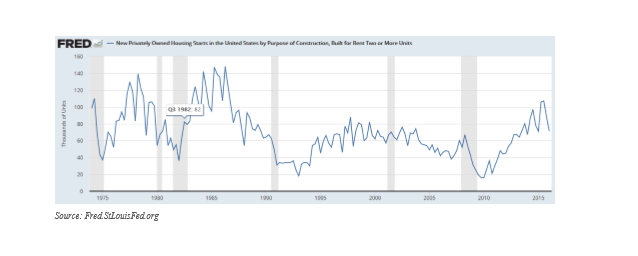

Figure 5. Fed Data Shows Construction Trends Ramping, But Not Out of Line with History

Source: Fred.StLouisFed.org

Different data set shows Apartment Construction Builds ramping but in line with history. Looking at a different data set on Rental Property construction, we see that construction output was well below typical (and likely below consumption rates) during 2010-2012, and that since then construction has roared back to life and is likely now filling some pent up demand for units. With Vacancy Rates still low, but starting to rise, we would expect to see New Construction Rental Starts begin to level off in coming quarters.

Figure 6. Apartment Prices are now Rising Dramatically, an Investment Risk

Source: Marcus and Millichap

Apartment Prices are rising dramatically in 2015 and 2016, an investment risk. Here we see that Apartment Prices (per door) have risen dramatically off the lows seen in 2009, and have even risen dramatically versus the prior cycle highs seen in 2006. Apartment prices per door topped out around $108K in the prior cycle peak of 2006, and have now risen up to about $140K per door, a roughly 30% price hike since the last economic cycle peak, and a nearly doubling off the 2009 lows. Versus 2009, we think that lower Cap-Rates account for roughly 40% of this move, while higher income per apartment (driven by higher rental rates) account for the remaining portion of apartment per-door price hikes. These increases are substantial and do increase investor risks as we continue to see big gains in the rear view mirror.

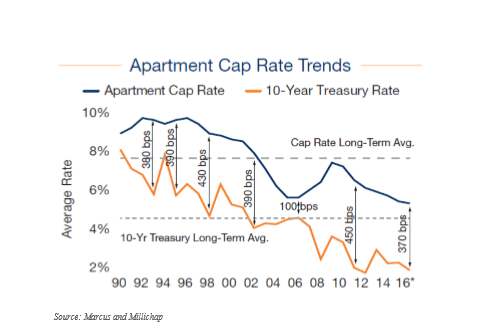

Figure 7. Cap Rate Trends Show Prices are About Typical Vs. 10-Year Treasury Rates

Source: Marcus and Millichap

Cap-Rates have contributed to rising Apartment prices. Are about where they should be As apartment sales prices on a per door basis have risen dramatically in recent years, we see that falling Cap-Rates account for a sizable portion of this increase. Indeed, Cap-Rates have fallen from about 7.7% in 2009 to about 5.5% today. This accounts for roughly 40% of the per-door apartment price hikes, but leaves rising net income as the other main driver of apartment price hikes.

Cap-Rates about appropriate given 10-year Treasury Rates. We think Cap-Rates are appropriate given the 10-year Treasury Yield (a 370 bps spread is typical compared to an average 400 bps spread since 1990). If one believes that interest rates should stay reasonably low given loose fiscal and monetary policies, as we do, then today’s low Cap-Rates do not seem to present as big a risk factor as others like ramping Apartment supply, a tapped out lower-income Consumer, or risks the broader economy softens.

Net Conclusion: Apartment market fundamentals remain solid, but broader economic risks remain. In short, we believe Apartment market fundamentals remain solid, but do continue to depend on broader economic and consumer driven trends that would weaken during an economic downturn. Rental Vacancy Rates look attractive compared to long-term trends, Rental Rate increases have been substantial (but should level off), and new supply is ramping to offset supply shortages that followed the Great Recession when building output was weak during 2010-2012. While we do see new supply as a bit of a risk to Vacancy Rates and Rental Rate growth, we do think that supply growth is getting the market back to a place of equilibrium after below-consumption output. We see high apartment prices on a per-door basis as one of the bigger risks to investing in apartments at present.

Follow Us On Social Media

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment